Is Wildfire Smoke Damage Covered by Insurance in Colorado?

Whether Colorado homeowners insurance covers wildfire smoke damage — coverage nuances, documentation that strengthens a claim, and working with adjusters.

Yes, in almost every case, with the right documentation

We have spent over two decades at Boulder Fire Restoration Pros answering the same critical question for Colorado Front Range residents. Yes, standard HO-3 and HO-5 policies treat smoke infiltration as a covered peril.

Many homeowners mistakenly assume that if the flames missed their property, their carrier will deny the claim.

This means you can get smoke only damage covered even when the structure itself never caught fire. What separates approved claims from denied ones is rarely the policy language itself.

The real dividing line is the quality of your documentation, paired with a professional wildfire smoke damage remediation scope that an adjuster can fund line by line. It helps to first recognize the signs of wildfire smoke infiltration so you know exactly what to document. Let’s look at the data, what it actually tells us, and explore a few practical ways to get your cleanup funded.

What’s typically covered

Our team consistently secures funding for four major categories of property recovery. A standard Colorado homeowner policy typically covers these essential areas of a wildfire smoke insurance claim.

- Dwelling damage: This includes HVAC decontamination, attic remediation, surface cleaning, and structural odor work. Recent 2025 data from HomeAdvisor shows that professional smoke damage restoration runs between $200 and $1,200 per room.

- Personal property: Your policy should handle soft contents that need professional cleaning or complete replacement.

- Additional living expenses (ALE): Temporary housing is covered if severe odors render the home uninhabitable. Colorado regulations have recently expanded ALE protections, sometimes granting up to 24 months of coverage during major declared disasters.

- Surface and air-quality testing: Insurers usually cover these initial assessments as a necessary documentation cost.

Sublimits and exclusions vary widely between carriers. Your declarations page remains the authoritative document for your specific policy limits.

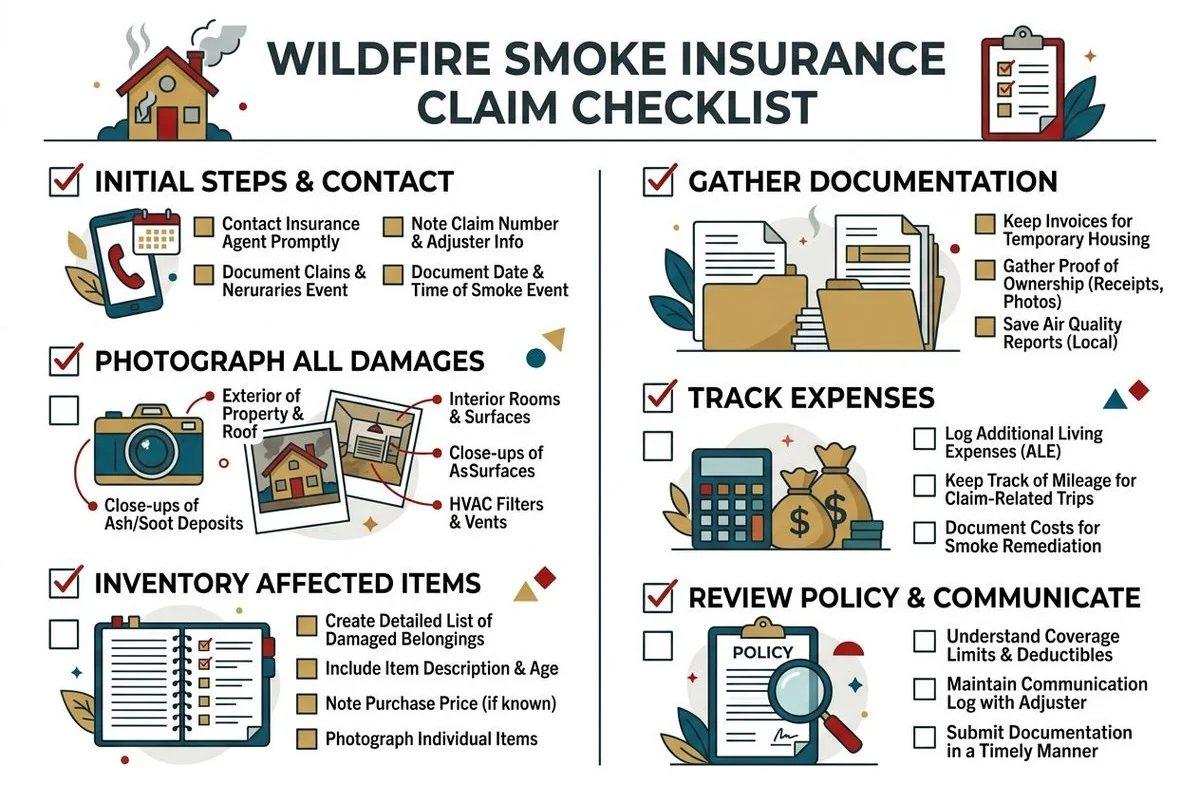

What strengthens a wildfire smoke claim

We always tell clients that objective data is the key to a fast approval. The five documentation pillars that get a wildfire smoke insurance claim approved rely entirely on hard evidence.

- Objective testing. Air-quality testing for PM2.5 and surface testing for soot particles give adjusters numerical evidence. Olfactory evidence is subjective, but EPA-recognized PM2.5 readings are impossible to ignore.

- Photo and video documentation. You must capture fine ash on horizontal surfaces, discolored HVAC filters, attic insulation contamination, and any visible film on hard surfaces.

- Scope of remediation in Xactimate. Adjusters scope losses using a software called Xactimate. Contractor scopes written in Xactimate align perfectly with the adjuster’s pricing and prevent prolonged disputes.

- Adherence to industry standards. The Institute of Inspection, Cleaning and Restoration Certification released the IICRC S770 standard in 2024 specifically for professional wildfire smoke damage. Citing this exact standard forces the carrier to fund a thorough, compliant cleanup.

- A clear timeline of events. Document exactly when the wildfire occurred, when smoke entered the building, when symptoms appeared, and when the assessment was performed.

What weakens a claim

Our staff reviews dozens of denied applications every year, and the same mistakes show up repeatedly. The pattern in under-paid claims usually comes down to a lack of preparation and hasty decisions.

- DIY cleaning before assessment. Once a homeowner wipes down visible surfaces, adjusters will aggressively question the original scope of the disaster. Photograph everything immediately before you attempt any cleaning.

- Skipping professional testing. Olfactory-only complaints face significantly more scrutiny than claims backed by laboratory results.

- Vague scope of work. Submitting a generic phrase like “smoke cleanup throughout home” without line-item detail invites massive scope reduction.

- Delayed reporting. Claims filed months after the event sometimes face causation questions. File within days of recognizing the infiltration to avoid giving the carrier an easy excuse.

Working with adjusters on infiltration scope

Adjusters typically arrive one to two weeks after you file your claim, and your preparation dictates the final payout. Colorado law CRS 10-3-1105 requires insurance companies to formally acknowledge these claims within 15 days of receipt. The on-site walkthrough is where the actual scope is established, making strong preparation absolutely essential.

We highly recommend treating the adjuster’s visit like a formal presentation. Your goal is to eliminate any guesswork about the extent of the contamination by following these exact steps.

- Have testing results ready. (We provide these as part of our initial assessment).

- Walk through every affected room together.

- Document HVAC filter condition and show the ductwork access points.

- Discuss attic and crawlspace contamination explicitly.

- Cover the soft content pack-out and the specific cleaning scope.

- Provide an Xactimate-aligned scope document at or shortly after the meeting.

When you have a contractor at the walkthrough who scopes in Xactimate, the conversation goes fast and alignment usually happens on the spot. Without an expert present, the adjuster may scope minimally. Homeowners then find themselves negotiating up from a very low starting point.

Direct billing and Colorado Law CO 10-4-120

Our billing department takes over the heavy lifting once the final scope is agreed upon. Colorado Law CO 10-4-120 strictly protects your right to choose a fire-specific specialist over the insurer’s preferred general restoration vendor. We bill the insurer directly for all covered work. You are only responsible for your deductible.

Everything else within the policy limits gets handled between the mitigation team and your carrier. Carriers are prohibited from intimidating or coercing you into using their network shops. Please see our insurance claims page for the complete details on your consumer rights.

If your claim is denied or under-paid

We regularly step in to rescue claims that a carrier initially rejected. Denials usually reflect light documentation, rather than strict policy exclusions.

Additional testing, a more detailed scope of work, and sometimes a public adjuster can turn the entire situation around.

Our team can easily help you with the necessary testing and detailed paperwork. For complicated disputes, experts coordinate directly with public adjusters and specialized attorneys to secure your funds.

Reach out today to schedule a comprehensive assessment and get your recovery back on track.

Frequently asked questions

Is wildfire smoke covered even if my house didn't burn? +

Most Colorado homeowner policies treat wildfire smoke infiltration as a covered peril regardless of whether your structure burned. Coverage depends on policy language, but smoke-only claims are routine and usually approved when documentation is strong.

How do I prove smoke damage to an adjuster? +

Three things: surface and air-quality testing for PM2.5 and soot particulate, photo and video documentation of fine ash deposition and HVAC contamination, and a professional scope of remediation work with Xactimate pricing.

What if my claim is denied? +

Strong documentation can support re-evaluation. Most denials stem from light evidence rather than policy language. We document rigorously specifically to prevent denials; if you're already in a denial situation, additional testing and a public adjuster can often turn the claim around.

Need help with fire or smoke damage in Boulder?

24/7 emergency response with a 60-minute guarantee across Boulder County. Call our team — we'll secure your property and walk you through the next steps.