You shouldn’t have to fight your insurer while you’re displaced

Are you feeling completely overwhelmed by the thought of handling a massive property loss? The day after a kitchen fire or electrical fire, you already have enough on your plate with housing, work, and taking care of your family.

Fire damage insurance claims are incredibly stressful, and the last thing you need is a crash course in homeowner policies.

You deserve to focus on getting your life back to normal.

Our team at Boulder Fire Restoration Pros has served the Colorado Front Range for over two decades, and we take the burden of insurance negotiations completely off your shoulders. This support means you can skip the multi-week arguments with an adjuster. We handle the heavy lifting through a few core steps:

- Notifying your insurance carrier correctly.

- Scoping the structural loss to exact Xactimate standards.

- Meeting the field adjuster directly on your site.

Every single project is documented to a level that stops disputes before they even start.

National data from 2026 shows that the average major residential fire claim tops $20,000, which means the stakes are incredibly high. The financial pressure is real, but you do not have to carry it alone.

So grab a cup of coffee, and let’s go through the exact steps together. We will show you everything you need to know to get your home restored quickly and fairly.

Colorado Law CO 10-4-120: the rule that protects you

When your insurer calls and recommends a preferred vendor for your fire restoration, that suggestion has a hidden financial relationship behind it. Preferred vendors usually get paid by the carrier based on volume agreements. These contracts include strict pricing concessions and scope expectations.

Those concessions rarely favor you or the safety of your home. They heavily favor the carrier’s loss ratio.

Colorado Law CO 10-4-120 protects your right to choose any qualified contractor for your fire restoration. This crucial 2007 state legislation explicitly forbids insurance companies from coercing or intimidating homeowners into using their preferred network.

You have the absolute freedom to select a fire specialist with deeper expertise and better equipment. We use this specific right routinely to protect homeowners like you. That means you can get a team with a real smoke odor elimination capability on your side.

Asserting your right is straightforward, because you simply tell your insurer in writing which contractor you have selected. If the desk adjuster pushes back, you just cite CO 10-4-120 and they have to comply.

Many homeowners feel pressured during those first phone calls. If your adjuster is pushing you to use their preferred vendor, that is the most important moment to reach out before you sign anything. We can help you draft that simple written notice.

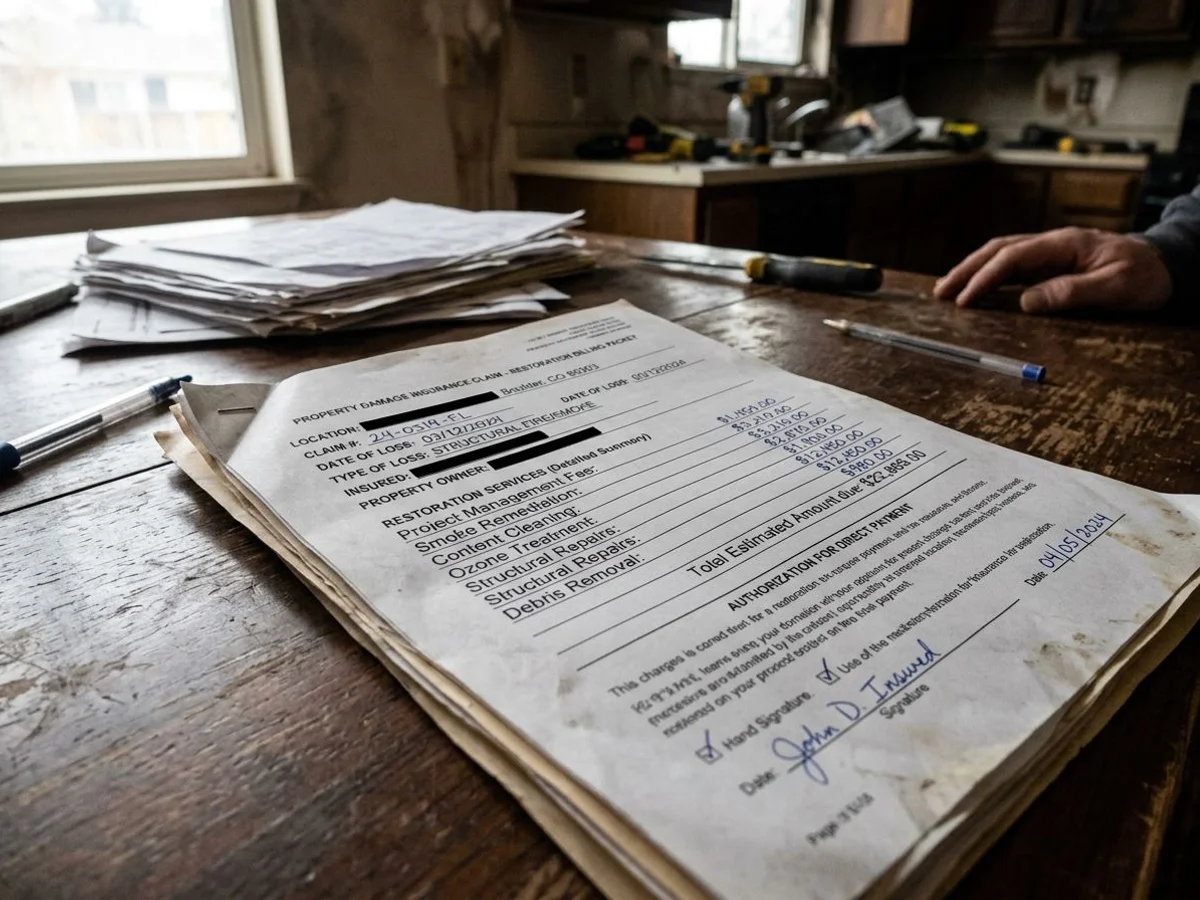

What goes into a strong insurance file

Adjusters approve claims much faster when the documentation is strong and the scope speaks their exact language. A complete file leaves no room for debate or unnecessary delays.

We build every claim file to meet the highest industry standards. Your adjuster will appreciate the clarity, which speeds up your approval timeline. We include several specific elements in every packet.

The Anatomy of a Bulletproof File

- Scope of loss in Xactimate. We use Xactimate because it commands an 80% market share among property insurance carriers in 2026. Every line item is priced directly to the adjuster’s localized pricing database. Submitting manual spreadsheets is the most common reason claims get delayed, so providing the native Verisk ESX format prevents unnecessary debates over rate.

- Photo documentation at every stage. Pre-mitigation, during cleanup, and at the final walkthrough all require visual proof. Hundreds of cloud-stored photos are shared directly with the adjuster.

- Line-item contents inventory. Every salvaged and non-salvaged item from content restoration is entered carefully. Each entry includes the specific category, condition, and a supporting photo.

- Daily moisture readings during dry-out. Strict documentation proves that the water extraction hit the required dry standard.

- Signed change orders. Anything missing from the original scope gets documented in writing and signed before the extra work happens.

Adjusters look at our carefully prepared files and the conversation gets very short. Scope alignment happens on the very first walkthrough. Payments process without a hitch, and the final close-out is completely clean.

What insurance typically covers for fire damage insurance claims

Most Colorado homeowner policies include several distinct categories of coverage. Knowing exactly what buckets of money are available helps you plan your recovery.

We can read your declarations page with you on day one to clarify your exact limits. This transparent review tells you exactly what to expect financially.

Your Primary Coverages Explained

- Dwelling coverage pays for structural damage and the physical rebuild of your home.

- Personal property coverage handles your physical contents. This usually includes strict sublimits on jewelry, electronics, and other specific high-value categories.

- Additional living expenses (ALE) covers the cost of temporary housing and extra food costs while your home is uninhabitable.

- Ordinance & law coverage pays for mandatory code-required upgrades during the rebuild. This is usually a 10% to 20% percentage rider.

- Trees and debris removal provides specific sublimits for the cleanup of fire-related debris on your actual property.

Colorado state law provides specific protections for displaced families under Bulletin B-5.35. Insurers are legally required to provide a minimum of 12 months of ALE coverage for a primary residence. They must also offer you the option to purchase up to 24 months of coverage.

| ALE Coverage Tier | Typical Time Limit | Standard Percentage Limit | Best Used For |

|---|---|---|---|

| Standard Coverage | 12 Months (CO Minimum) | 20% of Dwelling Limit | Minor to moderate fires requiring short-term relocation. |

| Extended Coverage | 24 Months (Optional) | 30% of Dwelling Limit | Major structural fires requiring complete property rebuilds. |

We see many homeowners forget to track their smaller out-of-pocket expenses. Keep every single receipt for meals and laundry, because those small daily charges add up quickly against your limits.

Specifics always vary by policy. We compare your documented damages against these exact coverage limits to maximize your approved repairs.

What we don’t do, and what we work alongside

We are a specialized fire restoration company, not a public adjuster and not an insurance attorney. For most standard claims, our documentation rigor is completely sufficient. You will likely never need to hire outside representation.

For unusually complex or highly contested claims, you may want to bring in a public adjuster or a lawyer. Public adjusters typically negotiate the claim on your behalf for a standard fee of 10% of the total settlement.

We coordinate with these professionals routinely. The detailed photo evidence we provide typically becomes the solid foundation of their legal case.

Expert Tip: If the insurance adjuster’s offered scope feels light, talk to us first. We can usually get it corrected through standard industry channels before anyone needs to escalate the situation.

If you are feeling overwhelmed by fire damage insurance claims, please call (303) 963-9968. We will review exactly where you are in the process. A clear path forward is just a phone call away.