Does Homeowners Insurance Cover Fire Damage in Colorado?

What Colorado homeowners insurance typically covers after a fire — structure, contents, smoke, deductibles, and additional living expenses.

Yes: does insurance cover fire damage colorado?

Our team has seen how the 2021 Marshall Fire fundamentally changed the way Colorado insurers handle property claims.

Every homeowners policy treats fire and smoke damage as standard covered perils. If you are searching to see does insurance cover fire damage colorado, the basic answer is always yes.

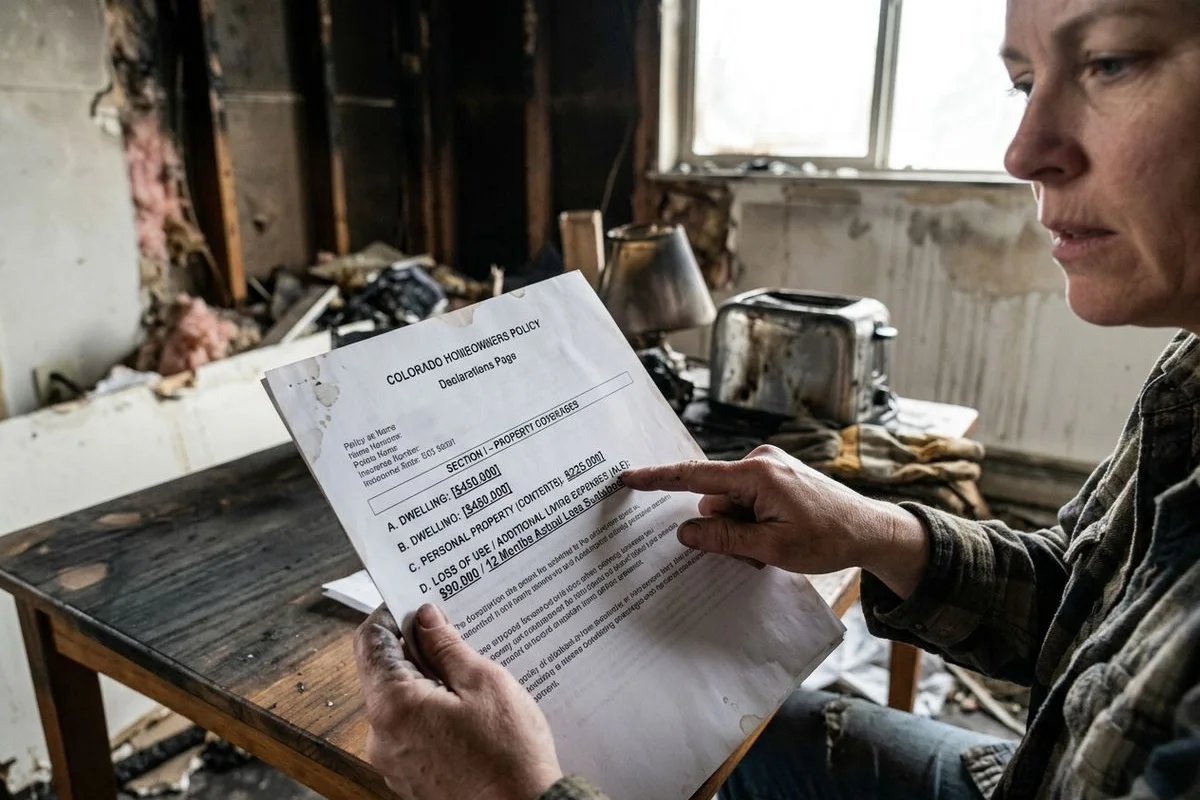

We constantly review these updated declarations pages to spot hidden coverage caps. The average state insurance premium jumped to around $4,000 in 2026. This price increase reflects a massive $141 billion in statewide wildfire risk.

We know that simply having a policy is rarely enough to guarantee a full rebuild. The important distinction most people miss is how sublimits restrict the actual payout. You must understand how these financial caps interact with current construction costs.

Our team is often asked what does fire policy cover under a standard HO-3 or HO-5 contract. The data tells a specific story about local rebuilding expenses. Here is the exact breakdown of limits and exclusions you will face.

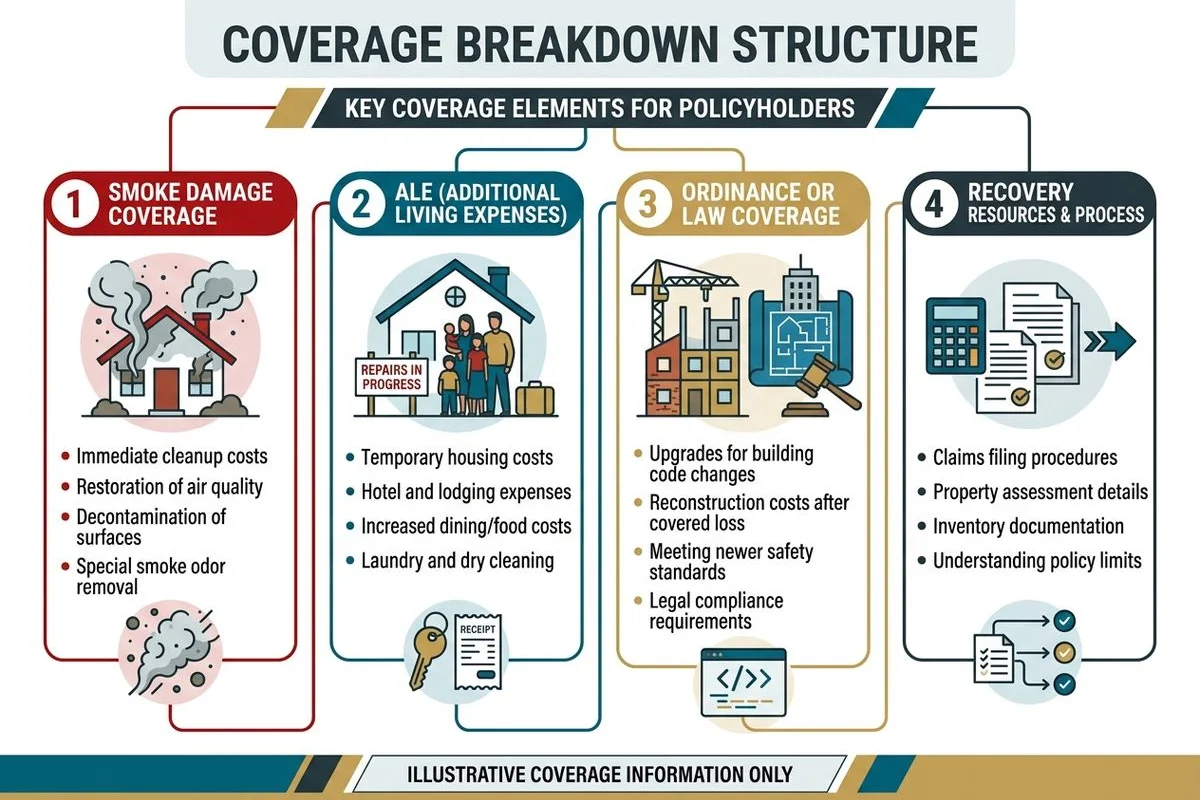

Dwelling coverage

Our experience shows that dwelling coverage pays directly for the structural damage to your home. This specific homeowners insurance fire coverage handles framing, drywall, electrical systems, and the roof. Limits are usually a stated dollar amount based on rebuild cost rather than market value.

We see a massive coverage gap in the current 2026 construction market. Standard Boulder County fire rebuilds now cost between $400 and $700 per square foot. A 2,500-square-foot property easily costs $1.5 million to reconstruct with builder-grade finishes.

We advise clients to demand an e2Value software appraisal to prove true replacement costs. A standard market appraisal will leave you severely underinsured. You need precise documentation to justify current labor and material rates.

Our estimators look for damage across several specific structural categories. The insurance company must pay to restore these exact components. These elements include the following features:

- Framing, flooring, and paint.

- HVAC and plumbing systems.

- Built-in cabinetry and permanent fixtures.

- Exterior siding, windows, and doors.

We strongly recommend updating your dwelling limit annually to match local inflation. The cost of raw materials in Colorado outpaces national averages. Under-insurance is a dangerous risk in the Front Range market.

Personal property coverage

Our adjusters know that personal property coverage pays to replace your damaged belongings. This limit is usually calculated as 50% to 75% of your total dwelling coverage. Standard policies handle furniture, electronics, clothing, and everyday kitchenware.

We always remind clients about a massive advantage hidden in Colorado law. State statutes require insurers to pay 65% of your personal property limits without a written inventory for total losses from a declared wildfire. This 2026 legal standard saves families months of exhausting documentation.

Our team tracks exactly how sublimits restrict specific high-value categories. Most policies cap payouts for targeted items unless you purchase a scheduled rider. Here is a comparison of standard contents versus restricted items.

| Standard Coverage Items | Common Sublimit Categories (Requires Rider) |

|---|---|

| Everyday clothing and shoes | High-end jewelry and watches |

| Basic living room furniture | Fine art and rare collectibles |

| Standard kitchen appliances | Firearms and related equipment |

We see homeowners lose thousands of dollars because they forget to schedule expensive electronics. Check your declarations page today to verify these specific caps. You must document sentimental items with photographs before a disaster strikes.

Additional Living Expenses (ALE)

Our project managers rely on Additional Living Expenses to pay for your displacement-related costs. This coverage handles hotel bills, short-term rentals, and extra food costs while your home is uninhabitable. The standard limit sits at 20% to 30% of your total dwelling coverage.

We warn every homeowner that rebuilding in Colorado takes far longer than expected. State law now mandates a minimum of 24 months of ALE coverage for declared fire disasters. High rent prices in Boulder County can drain a standard policy limit in just 14 months.

We recommend using specialized temporary housing vendors like ALE Solutions. These corporate services negotiate directly with your carrier to cover long-term leases. You must save every receipt for pet boarding, extra commuting miles, and restaurant meals.

Our billing specialists submit these specific displacement costs to adjusters. Keep track of these exact expenses to maximize your reimbursement. The approved displacement list includes:

- Short-term rental housing deposits and fees.

- Restaurant meals beyond your normal grocery budget.

- Pet-friendly housing premiums.

- Storage unit rentals for salvaged belongings.

- Replacement of daily essentials you left behind.

We submit these receipts periodically to keep the cash flowing. Waiting until the end of the project will cause massive out-of-pocket strain. The claims desk needs consistent documentation to approve the funds.

Smoke damage coverage

Our technicians ensure that standard fire policies cover smoke damage as part of the primary loss. This inclusion covers surface cleaning, HVAC decontamination, and complete odor elimination. The coverage applies to wildfire smoke infiltration even if flames never touched your property.

We know that the Colorado Division of Insurance strictly prohibits sub-limits that reduce ash damage payouts. Proving a pure smoke claim requires hard objective data. A professional PM2.5 particulate test costs around $300 and provides the exact evidence the carrier needs.

Proven cleaning techniques

We utilize several specific techniques to eliminate lingering odors. Masking the smell with sprays will never pass a final environmental clearance. The restoration industry relies on these proven methods.

We deploy thermal foggers to open building pores and neutralize deep-seated soot. Hydroxyl generators safely clean the air while you remain inside the home. Ozone treatments require the property to be completely vacant during the oxidation process.

Testing and documentation

Our field teams collect surface wipe samples to prove chemical contamination. You cannot rely on smell alone to win a dispute with the adjuster. Visual evidence of soot in the HVAC filter makes the strongest initial argument.

Ordinance & law coverage

Our estimators rely on Ordinance & law coverage to pay for mandatory code upgrades during the rebuild. This policy addition covers the financial gap between old construction methods and new municipal requirements. The rider usually provides an extra 10% to 25% on top of your dwelling limit.

We see this coverage save projects in jurisdictions with strict new environmental rules. The 2026 Boulder County BuildSmart and Wildland-Urban Interface regulations are incredibly rigorous. These codes mandate Class A fire-rated roofs, protected gutters, and ignition-resistant exterior siding.

We have watched these mandatory upgrades add between $6,000 and $18,000 to a standard property reconstruction. Older homes face massive structural changes just to pass the initial framing inspection. Without this specific rider, those extra construction costs come straight out of your pocket.

Our team verifies that the funds cover current electrical codes. Modern panels require AFCI, GFCI, and dedicated circuits for major appliances. Hardwired interconnected smoke alarms are now mandatory in all sleeping areas.

Tree and debris removal

Our site managers use the debris removal sublimit to fund the cleanup of ruined materials. This specific coverage handles the disposal of fallen trees, structural ash, and hazardous waste on the property. A typical policy includes a separate limit ranging from $500 to $5,000 for this exact task.

We warn property owners that total loss cleanup expenses frequently exceed these basic limits. Clearing a destroyed foundation in Colorado easily costs $15,000 due to strict landfill sorting regulations. Heavy equipment transport adds another layer of expense in mountain communities.

We advise checking if your carrier allows you to tap into the main dwelling fund once the sublimit is exhausted. Some premium policies provide an extra 5% debris allowance above the total structural cap. Securing a contractor early prevents toxic runoff from entering the local soil.

Common exclusions

Our reviewers always look for common exclusions that dictate what is typically not covered. The carrier will outright reject claims for pre-existing damage that has no relation to the recent fire. Arson committed by the insured is considered fraud and instantly voids the entire contract.

We constantly battle with adjusters over the definition of earth movement. Standard policies will deny claims if a post-fire mudslide damages the foundation. You must purchase a Difference in Conditions policy to protect against these secondary natural disasters.

Our specialists prepare clients for these other frequent denial categories. Make sure you understand these specific policy boundaries. Watch out for these unsupported losses:

- Ordinance and law expenses that exceed the designated rider limit.

- High-value jewelry or art lost without a scheduled rider.

- Reasonable wear and tear on the property.

- Vehicles parked in the garage during the event.

Your deductible is your out-of-pocket cost

Our financial coordinators explain that your deductible is your sole out-of-pocket cost for the project. Standard deductibles in Colorado range from $1,000 to $5,000 depending on your specific contract terms. You pay this set amount directly, and the carrier handles the remaining approved balance.

We process the rest of the funds through our direct billing system. While wind and hail policies are shifting to percentage-based deductibles, fire claims usually remain a flat fee. This stable pricing structure makes budgeting for a fire recovery much more predictable.

We collect the deductible upfront before dispatching the heavy mitigation equipment. The carrier subtracts this exact figure from their very first settlement check. You never have to pay multiple deductibles for a single continuous event.

What strengthens coverage

Our team wants you to be fully prepared before the next disaster hits. If your policy is up for renewal, you must discuss a few critical upgrades with your agent. When considering does insurance cover fire damage colorado, these specific changes will dictate your financial survival during a total loss.

We strongly urge clients to request these exact additions.

Make sure your new contract includes these essential protections. Check for these three critical items:

- True replacement cost coverage for both the dwelling and contents.

- An ordinance and law rider sized to current local building codes.

- An ALE limit and timeframe built for a realistic 24-month displacement.

We set our service standards based on these complex insurance requirements. For a deeper understanding of the paperwork, see how to file a fire damage insurance claim. For detailed project estimates, review the fire damage restoration cost in Colorado.

We are ready to help you restore your property the right way. Reach out to our mitigation experts today to schedule a comprehensive site inspection. Taking action now ensures your home is secure.

Frequently asked questions

Does homeowners insurance cover fire? +

Yes. Fire is a standard covered peril on virtually every Colorado homeowner policy. Coverage includes structure, contents, smoke damage, and additional living expenses while you're displaced.

Does it cover smoke damage too? +

Typically yes, including smoke-only damage where the structure didn't burn. Wildfire smoke infiltration is a covered loss on most standard policies — documentation matters for the specific scope.

Will the policy pay for somewhere to stay? +

Additional Living Expenses (ALE) coverage pays for displacement costs — hotel or rental housing, restaurant meals beyond normal grocery cost, pet boarding, and similar costs. Keep receipts for everything from hour one.

Need help with fire or smoke damage in Boulder?

24/7 emergency response with a 60-minute guarantee across Boulder County. Call our team — we'll secure your property and walk you through the next steps.